Analysis by Elijah Finn, Registered Investment Advisor (RIA) & Principal Analyst, Core Capital Report.

Introduction: Debunking the “Insurance as an Investment” Argument

In the complex landscape of financial products, Whole Life Insurance is often marketed as a dual-purpose tool: essential lifelong protection and a guaranteed, tax-advantaged investment. While the protection component is undeniable, the efficacy of the investment component—the Cash Value—is fiercely debated among fiduciary advisors.

As an RIA, my analysis focuses strictly on the opportunity cost and internal rate of return (IRR). For most investors building wealth, conflating insurance with investment is a structural mistake that erodes capital efficiency.

This data-driven analysis by Core Capital Report compares the typical performance of a Whole Life policy’s Cash Value against a common, low-cost alternative.

The Two Faces of Whole Life: Protection vs. Cash Value

A Whole Life policy premium is divided into three components:

- Cost of Insurance (COI): The true cost of the death benefit.

- Administrative Expenses and Commissions: Significant fees, particularly in the early years.

- Cash Value: The small remainder that is invested by the insurer. This is the “investment” component.

The Early-Year Drag

In the first 5–10 years, a substantial portion of your premium goes toward commissions and expenses. This means the Cash Value grows extremely slowly, often yielding an Internal Rate of Return (IRR) close to zero or even negative. Your money is not working efficiently when it is most needed to compound.

Finn’s Analysis: “The critical flaw in Whole Life as an investment is the fee structure. The high upfront costs act as an initial barrier, meaning you lose the crucial benefit of early-stage compounding. This is a structural drag on your overall wealth accumulation.”

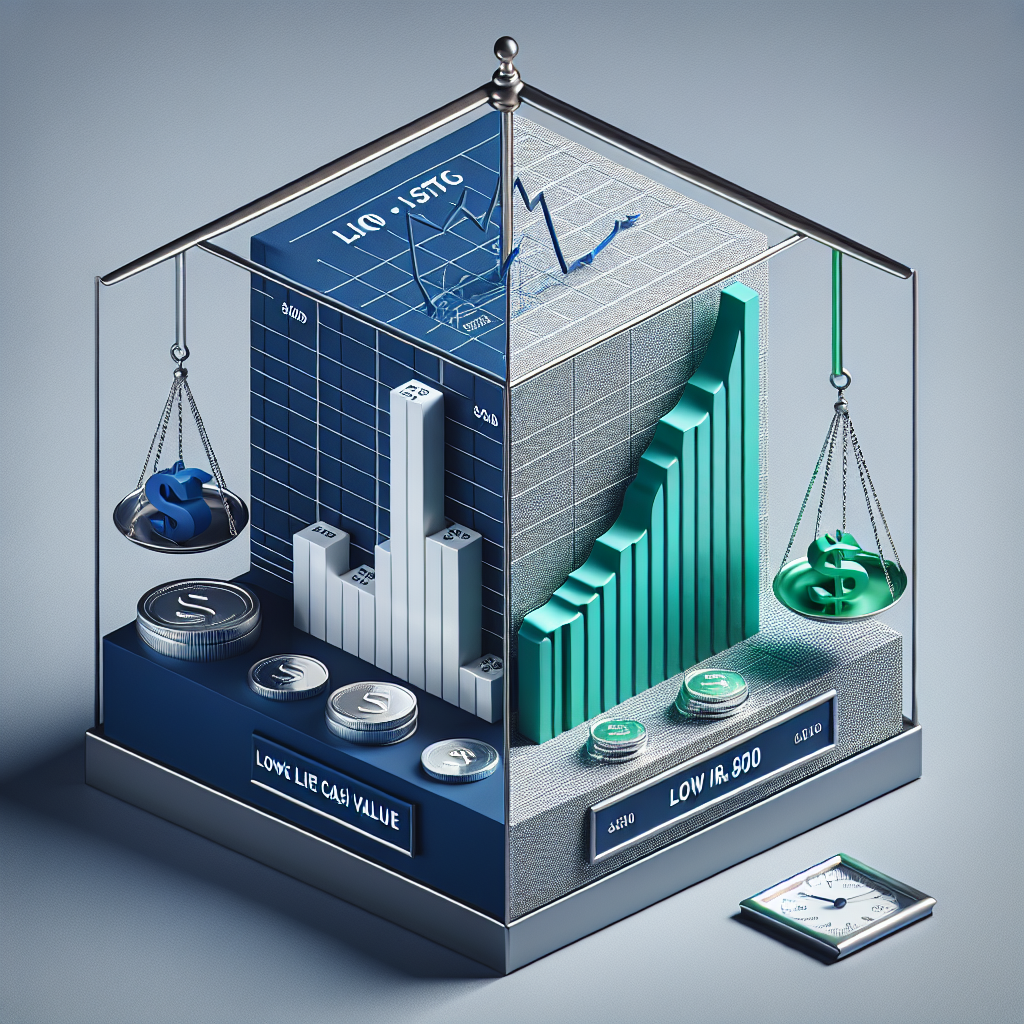

The Data Comparison: Whole Life IRR vs. S&P 500

The fiduciary argument against using Whole Life as an investment hinges on the opportunity cost—what your capital could be earning elsewhere. We compare the typical guaranteed growth rate of the Cash Value against a reliable, market-based benchmark.

Case Study: Whole Life vs. Buy Term and Invest the Difference (BTID)

| Metric | Typical Whole Life Policy (Ages 35–65) | BTID (Term Life + S&P 500 Index Fund) |

| Guaranteed IRR on Cash Value | 1.5% to 3.0% (Low, fixed rate) | N/A |

| Estimated Net IRR (After Fees) | 3.5% to 5.0% (Highly dependent on dividends) | 9.0% to 10.5% (Historical S&P 500 average) |

| Tax Advantage | Growth is tax-deferred; Loans can be tax-free. | Growth is taxable annually (unless in Roth IRA) |

| Capital Efficiency | LOW: Capital is locked up and illiquid. | HIGH: Capital is liquid and actively invested. |

Finn’s Analysis: “While the tax-deferred growth of Whole Life is a feature, its net internal rate of return (IRR) rarely exceeds 5% over 30 years. When you factor in the low cost of a Term Life policy and the historical 10% average return of a broad market index, the BTID strategy generates substantially more usable, taxable wealth for the average investor.”

When Does Whole Life Make Sense? (Strategic Exceptions)

Despite the poor investment returns, there are niche scenarios where Whole Life serves as a powerful wealth preservation tool for high-net-worth (HNW) individuals:

- Estate Planning: Using the policy to fund estate tax liabilities, guaranteeing tax-free liquidity when needed.

- Maxed-Out Tax Shelters: For HNW clients who have maximized 401(k)s, IRAs, and other tax-advantaged accounts, Whole Life provides another vehicle for tax-deferred accumulation without exposure to market risk.

- Guaranteed Liquidity: Accessing the Cash Value through policy loans can provide tax-free capital for business or real estate transactions without disturbing the investment portfolio.

Core Capital Report Conclusion

For the vast majority of individuals seeking to build wealth in their 30s and 40s, Whole Life Insurance is an inefficient investment vehicle. The high cost of commissions and the low guaranteed returns fundamentally violate the principle of maximizing capital efficiency.

Our recommendation remains clear: Buy Term Life Insurance to cover your risk exposure, and allocate the difference in premium cost toward a diversified, low-cost portfolio in a brokerage account.

Ready to calculate the true cost of your risk exposure? Secure a Term Life quote today.

Written by Elijah Finn, RIA.

⚠️ Financial Disclaimer & Advertising Disclosure

This article is for informational and educational purposes only. The content provided by Elijah Finn, RIA, does not constitute personalized financial, tax, or investment advice. Always consult with a qualified financial advisor before making complex financial decisions.

Advertising Disclosure: Core Capital Report uses Google AdSense to place advertising on this website. The presence of any advertisement does not imply endorsement of the advertised product or service by Core Capital Report.

Elijah Finn is a Registered Investment Advisor (RIA) and the Principal Analyst for Core Capital Report. With eight years of experience as a Portfolio Analyst at Morgan Stanley Wealth Management, Elijah specializes in translating complex financial strategies into clear, actionable advice for high-net-worth and middle-market clients. He holds an MBA in Finance from the University of Chicago Booth School of Business and maintains his Series 65 certification, adhering to a strict fiduciary standard in all analyses. His work focuses on maximizing long-term wealth through rigorous due diligence on investment vehicles, high-value credit cards, and robust insurance policies.