If you are deciding between term life and whole life insurance in 2026, the most important thing to understand is that these policies are built for different jobs. Term life is generally designed to provide coverage for a specific period, while whole life is a form of permanent insurance that is intended to stay in force for life and build cash value over time. The NAIC explains that term life is typically lower-cost coverage for a defined period, while cash value life insurance such as whole life can remain in force for life and includes a savings component.

That difference is why this is not really a “which one is better?” question. It is a which one fits the actual goal? question. If your main objective is to protect dependents during your working years, term life often fits that need well because it can provide more death-benefit coverage for less premium. If your goal is permanent coverage with built-in cash value, whole life may be the closer match, but the trade-off is usually much higher cost for the same death benefit. The Insurance Information Institute notes that permanent or whole life policies generally offer lifetime coverage but often charge higher premiums than term, meaning the death benefit can be smaller for the same amount of money.

The context also matters in 2026 because consumer demand for life insurance remains strong. LIMRA reported that U.S. individual life insurance new premium reached a record $17.5 billion in 2025, with whole life new premium up to $6.4 billion and term life new premium up to $3.1 billion. That tells you these products are still widely used, but popularity does not change the core decision: cost, purpose, and fit.

Bottom line

For many families, term life is the better fit when the goal is affordable income protection during the years when children, a spouse, or a mortgage depend on you. Whole life tends to make more sense only when you specifically want lifelong coverage, can comfortably afford much higher premiums, and understand that part of what you are paying for is permanent insurance plus cash value. The NAIC’s consumer guidance consistently frames term as lower-cost temporary protection and whole life as permanent, cash-value-based protection.

Who this article is for

This guide is especially useful if you are:

- buying life insurance for the first time,

- trying to protect a spouse, children, or mortgage,

- comparing lower-cost term coverage with more expensive permanent coverage,

- or wondering whether whole life is truly worth the extra premium.

It is also especially relevant if you have heard life insurance pitched as both “protection” and “an asset” and want to separate those two ideas clearly. The NAIC and III both describe term and whole life as different products with different purposes rather than interchangeable versions of the same thing.

What term life insurance is designed to do

Term life insurance is intended to provide a death benefit if you die during a specified term, such as 10, 20, or 30 years. The NAIC explains that term life is purchased for a set period and is generally meant to provide lower-cost coverage for a specific need or time horizon.

That makes term life especially relevant when your biggest risks are temporary but financially significant, such as:

- replacing income while children are still dependent,

- covering a mortgage,

- protecting a spouse who relies on your earnings,

- or supporting other major obligations that may decline over time.

In practical terms, term life is often the cleanest answer when the question is: How do I protect my family if I die during my highest-responsibility years? The NAIC specifically notes that term policies may be appropriate when you want lower-cost coverage for a defined period.

What whole life insurance is designed to do

Whole life is a type of permanent life insurance. The NAIC explains that cash value life insurance, including whole life, can remain in force for life and contains a savings component known as cash value. The III likewise describes whole life as permanent coverage that is built to remain in place for the insured’s lifetime.

That means whole life is generally built for people who want:

- lifelong death benefit protection,

- stable premiums,

- cash value accumulation inside the policy,

- and a product that combines insurance with a longer-term financial component.

But those features come with a real trade-off: higher premiums. The III notes that whole life typically costs more than term life, and because of that, the same budget usually buys less death benefit with whole life than it would with term.

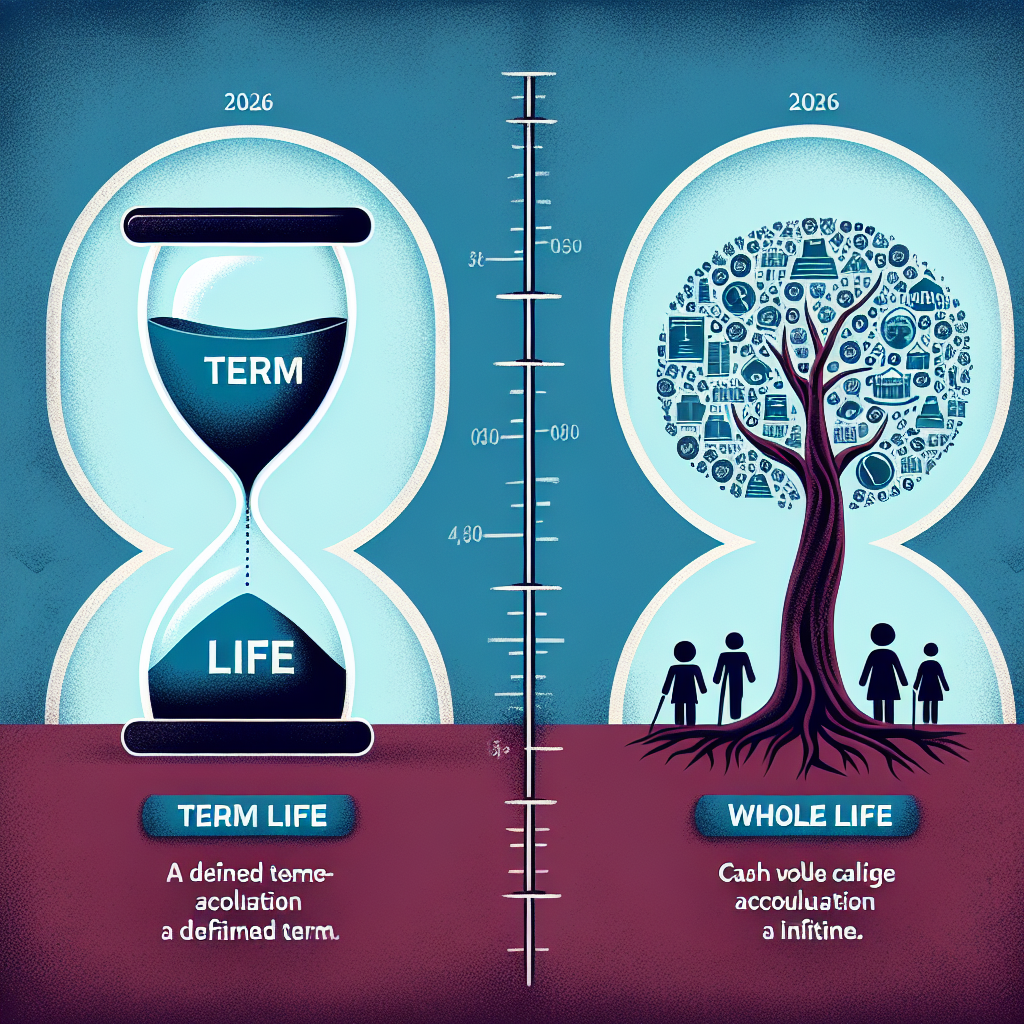

The biggest difference: temporary protection vs. permanent protection

If you strip away the sales language, this is the core comparison.

Term life

- coverage for a defined period,

- lower cost upfront,

- no cash value,

- best suited for temporary protection needs.

Whole life

- intended to last for life,

- significantly higher premiums,

- includes cash value,

- better suited for permanent coverage goals.

This is why term life and whole life should not be evaluated only by whether they both “pay a death benefit.” They solve different planning problems.

When term life is usually the smarter choice

For many households, term life is the more practical answer because it aligns well with the period when financial obligations are highest and budgets are most stretched.

Term life often makes the most sense if:

- you mainly need income replacement,

- you have children at home,

- you are carrying a mortgage,

- you want the largest death benefit for the lowest premium,

- or you are still building savings and cannot justify very high insurance costs.

The NAIC’s consumer guidance repeatedly emphasizes term’s role as lower-cost coverage for a specified period, which is exactly why it is often the strongest fit for younger families and working households.

When whole life may make sense

Whole life may make sense if your goal is not just temporary family protection but permanent insurance that you intend to keep for life.

Whole life may be a better fit if:

- you have a clear need for lifelong coverage,

- you value guaranteed permanence more than low cost,

- you understand how the cash value feature works,

- and you can comfortably afford the premium without sacrificing other priorities.

The important word there is comfortably. Whole life should not crowd out more urgent financial basics such as emergency savings, manageable debt, or retirement contributions. That is an editorial judgment, but it follows directly from the fact that whole life premiums are typically higher and therefore compete more directly with other household financial priorities. The III’s comparison supports that core cost trade-off.

Cost matters more than many buyers realize

This is where many life insurance decisions go wrong.

Because whole life generally costs more than term life, the question is not simply whether whole life has more features. The real question is whether those features justify the premium trade-off in your situation. The III states that whole life often charges higher premiums than term, and the NAIC explains that term is intended to provide lower-cost coverage for a set period.

That means a family with a limited monthly budget may face a very practical choice:

- a larger term policy that fully protects dependents,

- or a smaller whole life policy that lasts for life but may leave a protection gap.

For many families, underinsuring the core protection need just to buy permanent coverage is the bigger mistake.

The most common misunderstanding about whole life

The most common mistake is assuming whole life is simply “term life plus extra benefits.” It is not.

Whole life is a different product category with a different economic structure. The NAIC and III both make clear that permanent insurance includes cash value and lifetime coverage, which is why the premium structure is materially different from term.

That does not make whole life bad. It just means it should be bought for the right reason.

A policy designed for lifelong protection and cash value will usually not be the most efficient tool if your main problem is simple income replacement during your working years.

What life insurance demand in 2025 suggests, and what it does not

LIMRA reported record overall U.S. individual life insurance premium in 2025, with strong growth in whole life and continued growth in term life. Whole life represented 37% of the total life insurance market in 2025, while term life new premium rose 3% to $3.1 billion and policy count increased 2%.

That tells us two useful things:

- consumers still see value in both term and permanent coverage,

- and whole life is not a niche product with no demand.

But it does not tell us which one is right for a specific household. Market growth is not a personal recommendation. Your choice still needs to match your protection needs, budget, and long-term planning priorities.

How to choose between term and whole life

A practical way to decide is to ask what job you need the policy to do.

Choose term life when:

- your main goal is income replacement,

- your need is time-limited,

- budget matters a lot,

- and you want the most coverage per premium dollar.

Consider whole life when:

- you truly want permanent coverage,

- you understand and value the cash value component,

- you can afford higher premiums long term,

- and you are not sacrificing more urgent financial goals to make the policy work.

Common mistakes buyers make

1) Buying based on features instead of need

A policy with more features is not automatically better if it does not solve the right problem.

2) Underinsuring because whole life premiums are higher

If permanent coverage leads to a death benefit that is too small to protect the household, the family may be less protected than they think. The III’s cost comparison supports this concern because higher whole life premiums generally buy less death benefit for the same budget.

3) Treating term life as “less serious” insurance

Term life still provides a death benefit; it is not a lesser form of protection. It is simply designed for a defined time period. The NAIC is explicit on this point.

4) Assuming popularity equals suitability

LIMRA’s 2025 sales growth shows demand, not individualized fit. A record sales year does not answer your family’s planning question.

5) Confusing insurance with investing goals

Whole life includes cash value, but that does not mean it should automatically replace other core planning tools. This is an editorial caution grounded in the fact that whole life’s structure and cost are different from pure protection coverage.

A simple decision framework

If you want a practical shortcut, use this sequence:

- Do I mainly need protection during a specific window of time?

If yes, term life often fits better. - Do I need or want coverage that lasts my entire life?

If yes, whole life may deserve consideration. - Can I afford the higher premium without weakening other priorities?

This is critical because whole life generally costs more. - Am I solving a protection problem or buying complexity I do not need?

That is the question that prevents many expensive mismatches.

Bottom line

For many households in 2026, term life remains the most practical and cost-effective choice because it is built to provide affordable protection during the years when financial obligations are highest. Whole life can make sense, but usually only when the buyer specifically wants permanent coverage, understands the cash value trade-off, and can sustain the higher premium comfortably. The NAIC and III both frame these products in exactly those terms: term as lower-cost temporary protection, whole life as permanent coverage with cash value and higher cost.

The smartest choice is usually not the one with the most features. It is the one that fits the actual financial goal.

FAQs

Is term life insurance cheaper than whole life?

Generally yes. The NAIC describes term life as lower-cost coverage for a defined period, while the III notes that whole life typically charges higher premiums than term.

Does whole life insurance build cash value?

Yes. The NAIC explains that cash value life insurance, including whole life, includes a savings component that accumulates inside the policy.

Is term life better for families with children?

It often is, because families with temporary but significant income-replacement needs may benefit from lower-cost coverage for a set period. The NAIC specifically describes term as suited to coverage for a period such as 10 or 20 years.

Why do people still buy whole life if it costs more?

Some buyers want permanent coverage and value the cash value feature. LIMRA’s 2025 data shows whole life remained a major part of the U.S. individual life insurance market, with record new premium in 2025.

Is whole life always a bad idea?

No. It can make sense for some people, but it is usually most appropriate when there is a real need for permanent coverage and the buyer understands the cost trade-off. The NAIC and III both describe whole life as a distinct permanent product, not a universally superior one.

Disclaimer

This article is for educational purposes only and should not be treated as individualized legal, tax, insurance, or financial advice. Before choosing between term life and whole life, consider speaking with a licensed insurance professional, fiduciary financial advisor, or estate-planning professional.

Elijah Finn is a Registered Investment Advisor (RIA) and the Principal Analyst for Core Capital Report. With eight years of experience as a Portfolio Analyst at Morgan Stanley Wealth Management, Elijah specializes in translating complex financial strategies into clear, actionable advice for high-net-worth and middle-market clients. He holds an MBA in Finance from the University of Chicago Booth School of Business and maintains his Series 65 certification, adhering to a strict fiduciary standard in all analyses. His work focuses on maximizing long-term wealth through rigorous due diligence on investment vehicles, high-value credit cards, and robust insurance policies.