Analysis by Elijah Finn, Registered Investment Advisor (RIA) & Principal Analyst, Core Capital Report.

The Highest Standard in Financial Advice

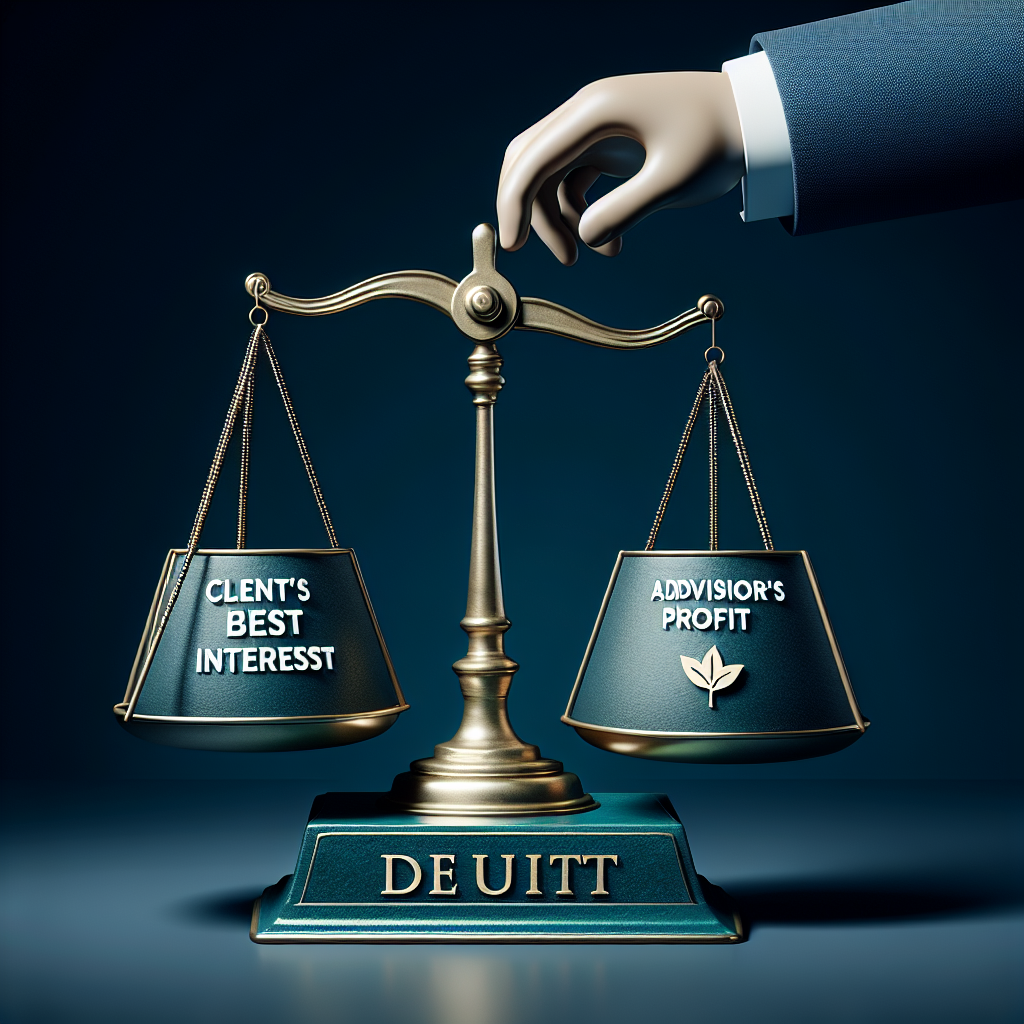

When seeking professional financial help, the most crucial question you can ask is: “Are you a fiduciary?”

A Fiduciary Financial Advisor is legally and ethically bound to put your best financial interests ahead of their own. This means they must disclose any conflicts of interest and recommend only the most suitable, low-cost investments, even if it means they earn a lower commission or fee.

In the U.S. financial landscape, the term “advisor” is loosely regulated. As an RIA, I believe that for comprehensive financial planning, the fiduciary standard is the only standard investors should accept. This guide details when you need a fiduciary and how to correctly identify one.

Fiduciary vs. Suitability: The Difference is Your Money

The distinction between a fiduciary and a non-fiduciary advisor (often referred to as a Broker or Registered Representative) is the difference between a consultant and a salesperson.

| Standard | Fiduciary (RIA, CFP®) | Suitability (Broker, Registered Rep) |

| Legal Obligation | Must act in the client’s best interest. | Must recommend products that are “suitable” for the client. |

| Compensation Focus | Fee-only (AUM or hourly) or Fee-based (Fees + Commission). | Commission-based (earns money from selling specific products). |

| Example Recommendation | Recommends a low-cost, 0.03% expense ratio index fund. | Recommends a higher-cost, actively managed fund with a 1.00% expense ratio and a commission, if it meets the client’s needs. |

Finn’s Analysis: “The ‘suitability’ standard allows a broker to recommend a product that makes them more money, even if a less expensive, better-performing alternative exists. The fiduciary standard demands the advisor recommend the most efficient capital solution for the client, period.”

When Do You Need a Fiduciary Financial Advisor?

You need a qualified fiduciary when your financial situation moves beyond basic saving and requires complex coordination.

- Mid-Career Wealth Accumulation (Ages 35-55): When you have significant assets in taxable accounts, 401(k)s, and Roth IRAs, and need tax-aware withdrawal and contribution strategies.

- Small Business Owners: When integrating business finances (like a Solo 401(k) or SEP IRA) with personal wealth and tax planning.

- Retirement Transition: When moving from the accumulation phase to the distribution phase, needing a sustainable withdrawal strategy (like adjusting the 4% Rule).

- Estate and Legacy Planning: When coordinating investment assets with legal documents (wills, trusts) requires expert, unbiased input.

The Fiduciary Vetting Checklist: 5 Key Questions to Ask

Before hiring any advisor, use this checklist to confirm their status and reveal potential conflicts of interest.

1. “Will you sign a written Fiduciary Oath for my account?”

- Why it Matters: Verbal assurances are insufficient. A commitment in writing is the strongest legal protection you can obtain. If they refuse, end the meeting.

2. “How are you compensated, and is that ‘Fee-Only’ or ‘Fee-Based’?”

- Fee-Only: Best case. They are paid only by the client (hourly or a percentage of Assets Under Management—AUM) and earn zero commissions.

- Fee-Based: Acceptable, but requires caution. They charge fees and can receive commissions. They must be extra vigilant about disclosing conflicts.

3. “What are the exact expense ratios of the funds you recommend?”

- Why it Matters: Fiduciaries prioritize low costs. If they recommend actively managed funds with expense ratios above 0.50% when a comparable index fund is available at 0.05%, they must clearly justify the value added by the higher cost.

4. “Do you have any conflicts of interest regarding product sales or referrals?”

- Why it Matters: A fiduciary must disclose all relationships. This reveals if they receive incentives for referring you to a specific insurance agent, lawyer, or brokerage product.

5. “What professional licenses and designations do you hold?”

- Why it Matters: Look for RIA (Registered Investment Advisor) status and the CFP® (Certified Financial Planner) designation. The CFP Board enforces a fiduciary standard when providing financial planning advice.

Making an Informed Investment in Advice

Hiring a financial advisor is a major decision—it is the ultimate investment in your financial guidance. By insisting on the fiduciary standard and utilizing this vetting checklist, you ensure that the person guiding your wealth is legally and ethically obligated to ensure your success comes first.

Don’t compromise on the fiduciary standard. Your long-term wealth depends on it.

Written by Elijah Finn, RIA.

⚠️ Financial Disclaimer & Advertising Disclosure

This article is for informational and educational purposes only. The content provided by Elijah Finn, RIA, does not constitute personalized financial, tax, or investment advice. Always consult with a qualified professional.

Advertising Disclosure: Core Capital Report uses Google AdSense to place advertising on this website. The presence of any advertisement does not imply endorsement of the advertised product or service by Core Capital Report.

Elijah Finn is a Registered Investment Advisor (RIA) and the Principal Analyst for Core Capital Report. With eight years of experience as a Portfolio Analyst at Morgan Stanley Wealth Management, Elijah specializes in translating complex financial strategies into clear, actionable advice for high-net-worth and middle-market clients. He holds an MBA in Finance from the University of Chicago Booth School of Business and maintains his Series 65 certification, adhering to a strict fiduciary standard in all analyses. His work focuses on maximizing long-term wealth through rigorous due diligence on investment vehicles, high-value credit cards, and robust insurance policies.