In the complex legal landscape of 2026, a single lawsuit can jeopardize the future of even the most successful enterprise. For small business owners and corporate executives alike, Commercial General Liability (CGL) Insurance is not just an optional expense; it is a foundational pillar of a robust risk management strategy. As inflation impacts legal costs and settlement amounts reach record highs, understanding the nuances of business liability coverage has never been more critical for maintaining long-term financial stability.

Whether you operate a burgeoning tech startup in Silicon Valley or a traditional manufacturing plant in the Midwest, your exposure to third-party claims—ranging from bodily injury to advertising personal injury—is constant. This comprehensive guide deep dives into the mechanics of CGL policies, ensuring you have the knowledge to secure the best protection at the most competitive rates.

1. What is Commercial General Liability Insurance?

At its core, Commercial General Liability Insurance is a comprehensive policy that protects business organizations against liability claims for bodily injury and property damage arising out of premises, operations, products, and completed operations.

The Scope of Coverage

A standard CGL policy provides coverage for several key areas:

- Premises Liability: Protection if a customer slips and falls at your place of business.

- Operations Liability: Coverage for damages caused by your business activities, whether on or off-site.

- Products and Completed Operations: Protection against claims that a product you sold or a service you completed caused injury or damage.

- Personal and Advertising Injury: Coverage for libel, slander, copyright infringement, or invasion of privacy in your marketing efforts.

2. Why CGL is Essential for Business Continuity

Many entrepreneurs mistake a General Liability policy for a “catch-all” solution. While it is broad, its primary value lies in the duty to defend. Even if a lawsuit against your company is meritless, the legal fees required to prove your innocence can exceed $50,000. A robust commercial insurance policy ensures that your carrier provides the legal defense team and covers the associated costs, preserving your working capital for actual business operations.

3. Deep Dive: Key Components of a CGL Policy

To maximize your insurance ROI, you must understand the technical definitions within your policy.

Occurrence vs. Claims-Made Policies

Most modern CGL policies are written on an occurrence basis. This means the policy covers claims resulting from accidents that happen during the policy period, regardless of when the claim is filed. On the other hand, claims-made policies only cover claims if both the incident and the filing of the claim occur while the policy is active. For long-term stability, occurrence-based coverage is typically preferred by high-growth firms.

Policy Limits: Aggregate vs. Per Occurrence

- Per Occurrence Limit: The maximum amount the insurer will pay for a single incident.

- General Aggregate Limit: The maximum amount the insurer will pay for all claims combined during the entire policy term (usually one year). In 2026, the standard recommendation for most SMBs is a $1 million per occurrence / $2 million aggregate limit, though high-risk industries may require commercial umbrella insurance for additional protection.

4. Top 5 Commercial Insurance Providers in 2026

Choosing the right carrier is as important as the coverage itself. Based on financial strength ratings (A.M. Best) and claims-handling reputation, these are the top providers:

1. Hiscox: Best for Small Businesses and Freelancers

Hiscox specializes in professional services and small-scale enterprises. They offer tailored General Liability packages that can be purchased online in minutes.

- Target Industry: Consulting, Marketing, and IT professionals.

2. Chubb: Best for Mid-Market and Large Enterprises

Chubb is synonymous with high-end corporate protection. Their “MasterPackage” policies provide extensive property and casualty insurance with global reach.

- Target Industry: Multinational corporations and high-revenue firms.

3. Travelers: Best for Diverse Industry Solutions

Travelers offers highly specialized policies for over 20+ industries. Their risk control services help businesses identify hazards before they lead to claims.

- Target Industry: Manufacturing, Construction, and Retail.

4. Progressive Commercial: Best for Ease of Access

While famous for auto insurance, Progressive has a massive footprint in the commercial lines market. Their network of agents makes it easy to bundle policies.

- Target Industry: Contractors and service-based small businesses.

5. Liberty Mutual: Best for Comprehensive Risk Management

Liberty Mutual provides deep technical expertise and excellent support for workers’ compensation and general liability integration.

- Target Industry: Wholesale and Logistics.

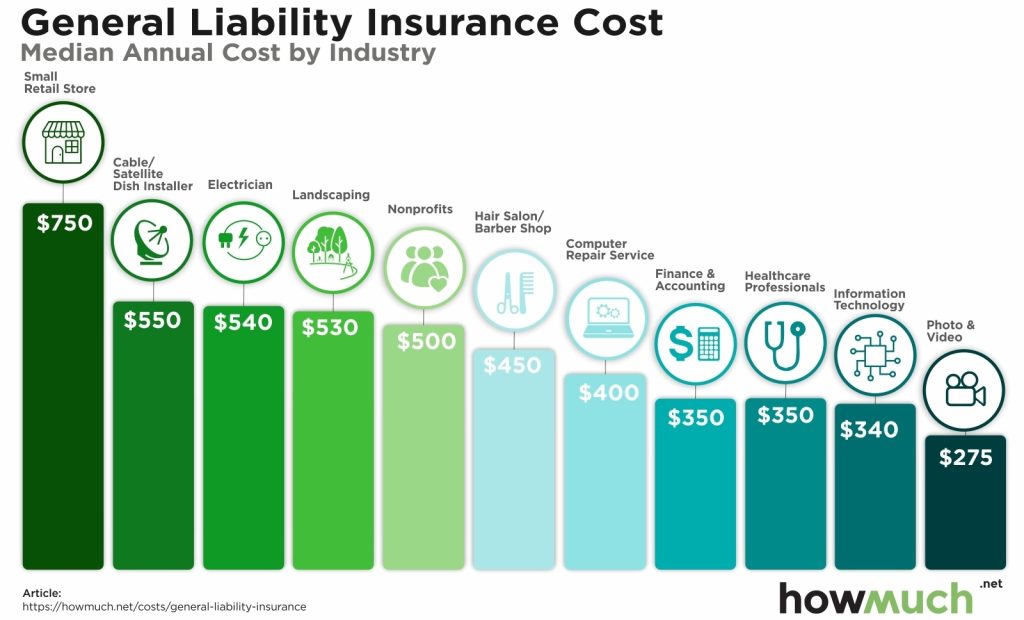

5. Estimating the Cost of Business Insurance

The question every CFO asks is: “How much will this cost?” In 2026, insurance premiums are calculated using sophisticated AI algorithms that analyze hundreds of data points.

Factors Influencing Your Premium:

- Industry Risk Class: A roofing company will pay significantly more than a graphic design firm due to the inherent physical risks.

- Business Location: Rates vary by state due to differing legal environments (e.g., litigation-heavy states like California or New York).

- Claims History: A “clean” record is the best way to secure low rates.

- Revenue and Payroll: Larger companies represent more “exposure” for the insurer.

6. Common Exclusions: What CGL Does NOT Cover

To avoid a catastrophic financial surprise, you must know where your CGL policy ends. Generally, CGL does not cover:

- Professional Errors (E&O): If you give bad advice that costs a client money, you need Professional Liability Insurance.

- Employee Injuries: This requires Workers’ Compensation.

- Cyber Attacks: Data breaches and hacking require a dedicated Cyber Liability Policy.

- Commercial Auto: Vehicles used for business must be insured under a separate commercial auto policy.

7. Strategic Integration: Linking CGL with Business Growth

Smart CEOs view insurance as an enabler of growth. Many large clients and government contracts require a Certificate of Insurance (COI) with specific limits before you can even bid on a project. Having your Commercial General Liability in order allows you to compete for higher-value contracts and secures your position in the B2B supply chain.

8. Managing Your Policy: The Importance of Annual Reviews

As your business evolves, your insurance must evolve with it. If you launch a new product line or open a second location, your old policy may leave you exposed. An annual review with your insurance broker ensures that your limits are adequate and that you are taking advantage of any new discounts available in the 2026 market.

9. The Impact of “Social Inflation” on Insurance

A trend we are closely monitoring at Core Capital Report is social inflation—the rising cost of insurance claims due to increased litigation and larger jury awards. To combat this, businesses are increasingly turning to Risk Retention Groups and higher deductibles to keep their monthly premiums manageable without sacrificing core protection.

10. Conclusion: Securing Your Enterprise

Navigating the world of Commercial General Liability Insurance can be daunting, but it is an essential part of the modern business journey. By partnering with the right carrier and understanding the fine print of your coverage, you protect not just your physical assets, but the intellectual and financial capital you have worked so hard to build.

While insurance protects your assets, maintaining cash flow is equally vital. Read our guide on [Fast Invoice Factoring]

Elijah Finn is a Registered Investment Advisor (RIA) and the Principal Analyst for Core Capital Report. With eight years of experience as a Portfolio Analyst at Morgan Stanley Wealth Management, Elijah specializes in translating complex financial strategies into clear, actionable advice for high-net-worth and middle-market clients. He holds an MBA in Finance from the University of Chicago Booth School of Business and maintains his Series 65 certification, adhering to a strict fiduciary standard in all analyses. His work focuses on maximizing long-term wealth through rigorous due diligence on investment vehicles, high-value credit cards, and robust insurance policies.